Toothless talking shop or shadow standard-setter?

On September 22, 2019, 132 banks came together to launch the UN Principles for Responsible Banking (PRB). The initiative, encompassing lenders of all kinds and sizes from around the world, was trumpeted as the means by which banks would contribute to the fulfillment of both the Paris Agreement and the UN Sustainable Development Goals (SDGs).

A year on, the coalition is now over 185 banks strong, and recently agreed to a new governance structure. The hope is the PRB can succeed where previous efforts have failed in getting banks to collectively tackle climate-related risks and maximise their positive impact on society and the environment.

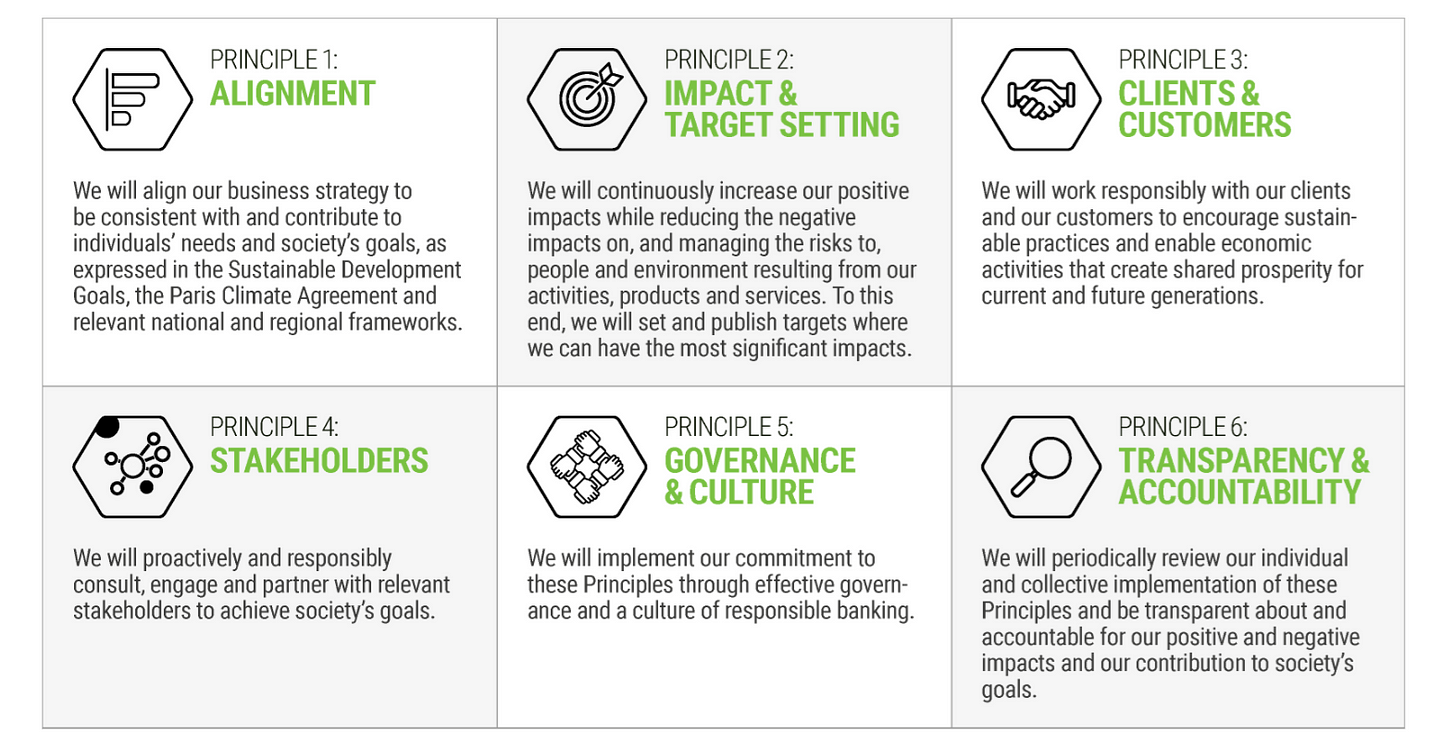

Members commit to six principles (below) and to report on their implementation at periodic intervals. The new governance structure, rolled out in June, also makes members accountable to a 12-member banking board — which will be the final judge and arbiter on whether they are pulling their weight.

Source: UNEP FI

“Our principles do have teeth, and through a review process we will be able to flag cases where not enough progress is being made, which will trigger engagement and ultimately the possibility to remove a bank from the list of signatories” says Simone Dettling, banking team lead at the UN.

This should distinguish the PRB from other frameworks where targets aren’t binding and progress isn’t monitored — and to which members consequently pay lip service to. “Banks themselves are tired of being in initiatives where they are doing things but others are not, which discredits them as a whole. If you have a tonne of free riders, your own work as an individual bank is not going to be credible,” says Dettling.

Stirrings of a standard-setter

The PRB, and the organisation being built around it, could become much more than a joint statement of shared goals, however. Members see its potential as a central hub for coordinating the banking industry’s response to climate risks and systematising the deployment of sustainable finance.

“The more alignment, the more initiatives we use in common, the easier it will be for all members to steer in the same direction,” says Anders Langworth, head of sustainable finance at Nordea and a member of the PRB banking board.

Just as the club of financial watchdogs that make up the Network for Greening the Financial System (NGFS) is fast developing into a climate-focused iteration of the supranational Basel Committee on Banking Supervision, the PRB has the makings of an industry-led standard-setter that could work in concert with regulators, clients and governments alike. “I feel like the PRB could be the preeminent platform for advancing social and environmental progress within the banking system,” says Elsa Palanza, global head of sustainability and ESG at Barclays and another member of the PRB banking board.

The group has shown some promise in this area already. Members say they have benefited from the connections forged last September in handling the devastating economic fallout of the coronavirus pandemic.

“In response to Covid-19, banks around the world undertook a myriad of actions, each tailored to their specific market segment and geography,” says Hervé Duteil, chief sustainability officer at BNP Paribas Americas.

“The PRB coalition proved to be a powerful forum to exchange information on how different banks adapted their business measures … in line with principle three of the initiative to work responsibly with clients and customers. Retail banks and commercial banks each had their own way to build the resilience of people, families, SMEs and the economic system, and all could learn from one another,” he adds.

In the context of climate risk and impact finance, the PRB offers access to a wealth of expertise and case studies for firms new to the world of sustainable banking. Those further along on their journey have also benefited from the network when grappling with the tougher challenges of portfolio alignment and client monitoring.

“The main benefit is the peer learning we are able to have through different working groups,” says Nordea’s Langworth. “The more advanced you are, and the further down the line you have come with the calculations, the more complex it becomes. We have resources, but we are getting a lot of shared knowledge and valuable contributions to complete these big, complex calculations and tools with others banks instead of having to do it ourselves.”

A subset of PRB banks have even formed a makeshift vanguard committed to finding the most effective ways for firms to operationalise the principles. The Collective Commitment to Climate Action (CCCA) is a group of 38 signatories dedicated to aligning their portfolios with a Paris Agreement-compliant temperature trajectory and revamping their products, services and client relationships to bring about a climate-neutral economy.

“The idea is to help us map out our collective strategy with respect to how people are thinking about current work and priorities,” says Ivan Frishberg, co-chair of the CCCA working group on reporting and target setting, and vice president of sustainable banking at Amalgamated Bank.

The CCCA members committed to report back annually on their individual progress, and biennially on their collective progress, with the first wave of status updates expected this month.

Sorting the toolbox

Beyond data-gathering and fact-finding, the PRB is also in the business of evaluating the tools and methodologies that can help member banks fulfill their commitments.

“What the sector needs to have is a few really strong and common frameworks to look at and use rather than have 10-20 different ones, and to have a debate over which ones [are] best … Going forward if you have too many options for calculation methods, it will be very difficult to set proper targets. Consistency is needed,” says Langworth.

This is not to say the PRB will be actively ‘picking winners’. Still, with its long membership roster and the imprimatur provided by the UN, it has the leverage to nudge signatories — and the industry at large — towards certain practices. The group already has a portfolio impact analysis tool, launched in March, to help members analyse the impacts of their retail and wholesale portfolios. Banks affiliated with the PRB have also piloted the Paris Agreement Capital Transition Assessment (PACTA) tool and contributed to a new version that can gauge the climate alignment of their business lending portfolios.

Over time, it may make sense for PRB members to coalesce around common practices, though the variety of banks involved makes rigid standardisation a non-starter. What makes sense for VanCity — a tiny Canadian lender with $27 billion in assets under management — will not do for Citi, a systemically-important bank about 27x its size.

Small community banks, like the former, may find the framework designed by the Partnership for Carbon Accounting Financials (PCAF) is all they need to measure and disclose their financed emissions and put together a decarbonisation plan — thereby fulfilling PRB principles one, two and six.

Sprawling multinational investment banks, on the other hand, will have to use an array of tools — the Poseidon Principles, perhaps, to measure and monitor the climate alignment of their shipping portfolios, and Science Based Targets to organise the decarbonisation of their securities holdings.

The PRB therefore has to be broad enough to encompass all the methodologies required to get every member on the road to Paris and the SDGs.

“One thing that differentiates the PRB is it’s a strategic framework,” says Palanza. “You can think of [it] as the foundational platform that underpins all these other tools which help assess your banking model”.

Certain observers see more strategic fuzziness than focus in the way the principles have been put together, though. “The PRB principles are too generalised,” says Suborna Barua, assistant professor at the Department of International Business at the University of Dhaka and author of Principles of Green Banking.

“It just says ‘you have to do this’, but doesn’t say ‘how’ — and the ‘how’ question is very important. For example, signatories are supposed to run an impact assessment [but] each bank could run an impact assessment its own individual way. That could create another kind of problem, because it’s not the same standard implemented across banks,” he explains.

The PRB does offer a blueprint to members, however, on fulfilling the principles through a guidance document published earlier this year. Though not prescriptive, the document at least clearly explains minimum requirements and suggested measures.

One direction

Debating the best route to a sustainable banking system is one thing. Agreeing on what this system should look like is another. Yes, PRB signatories agree to “strategically align” their businesses with Paris the SDGs — but this means different things to different stakeholders.

“For us, PRB banks can’t ignore fossil fuels,” says Daisy Termorshuizen, climate campaigner at BankTrack, an international civil society organisation (CSO) committed to following lenders’ involvement financing environmentally-damaging activities. “The most important thing from our perspective is that if you are a PRB bank, you commit to align with the Paris Agreement and therefore have to stop financing fossil fuels.”

Together with 59 other CSOs, BankTrack endorsed its own ‘Principles for Paris-aligned financial institutions’ on September 16 — a list of rigid prescriptions that juxtapose with the PRB.

The Paris-aligned principles prohibit banks from funding any expansion of fossil fuel extraction and exploration, and demand they phase out coal financing entirely by 2030 for OECD countries and by 2040 everywhere else. The present coal policies of certain PRB member banks (such as Mizuho) fall far short of this target.

In addition, the CSO’s principles tell banks they cannot rely on ‘net zero accounting’, whereby carbon-emitting activities are ‘offset’ on banks’ balance sheets by the financing of carbon-extractive technologies, like reforestation. This requirement puts the principles at odds with PRB signatories, like Barclays, which have made net zero an important plank of their climate strategy.

The roll out of the Paris-aligned principles is a conscious challenge to the PRB, and evidence that environmentalist groups are far from convinced the group will be able to bring about effective change.

Another concern raised by BankTrack is that the PRB is overly generous when it comes to deadlines: “It’s difficult to know what progress has been made because the timeline does not require the banks to show progress for a long time. Banks have up to four years to demonstrate their implementation and don’t have to report on their progress to the rest of the group for 18 months [after joining],” Termorshuizen explains.

Members say these timelines were decided so as not to scare away banks unversed in climate risk and impact finance. Says Langworth: “If the early requirements are too strict on the timing, I think the threshold for a bank with a low maturity to join will be too high. Then the PRB will have the opposite effect from that desired. Initially it’s good we have enough time for many banks to join.”

The PRB’s new governance structure is also intended to make sure these deadlines are enforced. The banking board’s ability to kick out members that are unable or unwilling to address their commitments in a timely manner puts pressure on signatories to take them seriously.

Barua isn’t convinced delisting is an effective enough inducement, however. “There is no ‘reward’ for being a part of PRB that you’d lose. If I’m a bank and sign the PRB today, that could have a positive impact on my business volume. Then if I were delisted, this new business may be negatively affected. But that’s not the situation now.”

A helping hand

The governance shake-up adds another layer of accountability, though, in the form of a 12-member Civil Society Advisory Body (CSAB) to “guide and support” implementation of the principles and provide an “independent view” on members’ collective progress.

“The main purpose we wanted to achieve by having this board is to ensure we have a solid feedback loop, and make sure that we’re not sitting on a banking board and only discussing our main topics and targets,” says Langworth. “Having a constant dialogue with key stakeholders — regulators, customers, NGOs — in a formal manner allows us to align at a global level. It will also push banks to have these dialogues on the local level. That, in the end, is what’s needed, because if we have a civil society board with a few members from around the world, they will not be able to talk for all regions and trickle down information for all regions.”

This concern, that the CSAB could become a cloistered talking shop, is one voiced from outside the PRB too — but from a different perspective. “Our worry is that civil society organisations will be picked that are friendly to the banks and don’t represent all voices,” says BankTrack’s Termorshuizen.

Others think the body has the wrong purpose. Barua says the true role of civil society should be in getting the word out on the PRB, and encouraging users of financial services to prefer the environmentally-responsible banks that comprise its membership.

“The other way they could help is by putting pressure on governments to ask them to take out regulations on environmental protection and make them more effective,” he adds.

American exceptionalism

Looking ahead, members expect the PRB to focus on growing the network, sharing best practices, and digesting the findings of its unofficial vanguard — the CCCA banks.

One additional near-term objective, voiced by several members, is to get more large US banks on board. Right now, Citi is the only US systemically important bank signatory. However, in recent weeks, top firms Morgan Stanley and Bank of America have joined the Partnership for Carbon Accounting Financials, perhaps indicating that Wall Street is warming to the idea of multilateral climate initiatives. The expectation of a number of people interviewed by Climate Risk Review is that more US banks will join the PRB if President Trump loses the White House.

More members means more expertise, more burden-sharing, and faster collective progress towards the PRB’s goals. Advocates make the point, though, that its work won’t stop once the principles are all integrated within banks’ processes — the PRB will simply evolve.

“A lot of banking initiatives are ‘static’. There are thresholds to get over, and once a firm hurdles those, then the initiative stales, and becomes more like a trade association. The PRB offers much more of a ‘ramp’ than a ‘bar’. Members have to continually progress. First, a bank has to see where they can have major impacts, then figure out how the can achieve these, set targets and report on them transparently. Then they can review and repeat the process,” says James Vaccaro, executive director of the Climate Safe Lending Network and senior advisor to Triodos Bank, a PRB member.